Institutional Memory and the Neuralyzer

‘Institutional memory’ is typically thought of as an organization’s collected knowledge of facts, experiences and concepts. Knowledge is often forgotten, shaped, interpreted and reinterpreted over time. Sometimes institutional memory is enshrined in icons like logos, buildings, or mythologies, which serve as mechanisms to ensconce institutional knowledge into a an identity, or even an ideology.

Most of us acknowledge that storytelling has always been the key to culture – from passing down stored knowledge like tribal history, specific technical knowledge (how to build something) or cultural customs. We are predominantly evolved to learn and communicate through narrative. Even one of the oldest stories we know, “The Epic of Gilgamesh” has the same literary themes you’ll see in your favourite Netflix show: A king and a rival fight, become allies, set out on a hero quest, one of them dies, a reprisal second quest begins, and the true nature of reality presents itself.

“Nothing ages faster than yesterday’s vision of the future”

There are natural reasons for institutional memory to change and fade over time. As resource optimizing mammals, we are wired to focus brain cycles and calories on whatever seems the most pressing to survival and well being. Employees with knowledge leave organizations, records aren’t read or disappear and memories fade. Managers focus on beating last quarter’s sales figures and hiring employees that bring in revenue come hell or high water.

One narrative common in economic history is that the German Bundesbank had a stored set of memories directly linked to the economic experience of the hyper-inflationary Weimar Republic. This is tethered to the narrative that the German people had also developed a national psyche that orbited around the perils of hyperinflation, even post WWII. Google ‘Weimar Republic’ and take a look at the images associated with the topic. They look the image below.

German newspapers and national narrative post WWII and pre-ECB were very sympathetic to the Bundesbank’s hawkish execution of its price stability mandate.

There were A LOT of terrible consequences for the German people that were compounding as reparations went unpaid. The French occupied the Ruhr, limiting access to coal and signalling that the Versailles Treaty would be enforced. The Republic used extensive propaganda in an effort to conceal the rate of price inflation from the public, closing stock exchanges, instating price controls, and blaming both the WWI defeat and the horrific economic condition on deserting soldiers (who weren’t being paid regularly during the rebuilding of Germany). After numerous coups and assassinations, the 1932 Reichstag elections established the NSDAP as the largest party in parliament and set the stage for a series of events that would eventually set Europe on fire.

So did institutional memory influence the policies of the Bundesbank in the ’57 to ’90 period? Probably. Popular pictures like the one below, of people using bank notes to wallpaper their houses and for use as coffee tables had become a part of the German collective memory of pre-WW2.

Germany didn’t finish paying their WWI reparations until 2010! Trying to decipher the status of WWII reparations is even more complex, with multiple amendments since the 40’s, and as recent as 5 years ago Greece and Israel both claimed that Germany owed further payments. Decades of Soviet occupancy was the cherry on top of a multi decade tragedy for the German people.

Most historical narrative from academia does link the national political instability exacerbated by 1920’s hyperinflation to the rise of the Nazi party. And has linear narrative preferring apes, it makes sense, after all it came right before. Digging deeper on the topic is PhD thesis material, and way over my pay grade, but it’s safe to say that the printing presses were at a minimum a destabilizing force, what Soros would call positive reflexivity.

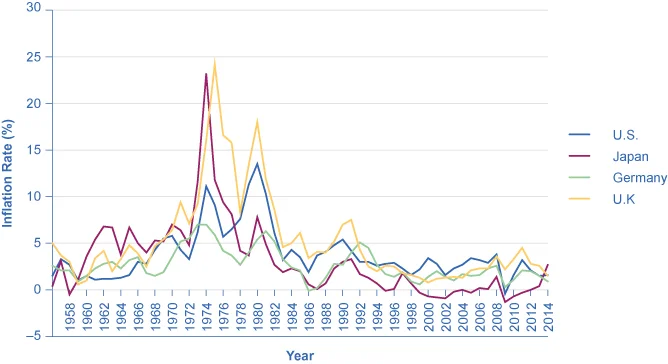

The below chart illustrates the success of the Bundesbank in capping 1970’s inflation.

Image credit: Figure 2 in "How the U.S. and Other Countries Experience Inflation" by OpenStaxCollege, CC BY 4.0

By the time the ECB was established in 1998 and the next phase of the European project was firmly underway, effectively moving monetary policy decisions to the single mandate ECB, the developed world had not seen anything that had resembled 70’s, or even ‘80s inflation. If the lessons of the 1920’s and 1970’s had left some remnant of institutional memory within German central banking by the late 1990’s, surely this at least the beginning of the end.

The BIS did a study in 2003 entitled “The institutional memory hypothesis and the procyclicality of bank lending behavior” with the goal of determining (a) is bank credit creation procyclical? (hint: yes), and (b) does this occur because of institutional memory, in particular how it changes throughout the business cycle (hint: yes, partly). The study considers the idea that during a cycle boom, overly optimistic lending officers ease credit standards and get caught up in some classic behavioral finance traps. Secondly, few officers or executives from the previous cycle were still in the organization – they had lost institutional memory. The net effect is that bank lending in this manner exacerbates business cycles, increases systemic risks, and makes regulators jobs harder. https://www.bis.org/publ/work125.pdf

This describes the natural decay of institutional memory. This can happen at different rates with different consequences depending on the type of organization and exogenous environment. With each passing year since the GFC, less PMs, risk managers and even CIOs have experienced risk management in a non-centrally planned environment. Talk about modelling errors being institutionalized! As with each passing generation of Germans, the power of the cautionary tale of the destructive nature of hyperinflation is gradually diluted and slowly fades away. It is not ‘deleted’ from history, instead is subject to the human phenomenon of rationalizing resources to a threat that hasn’t materialized in generations.

I recall working on an institutional trading desk in 2008, and some of the more well read senior guys on the desk cited ‘moral hazard’ as a major determinant of how the crisis would play out. They were wrong. Few in the mainstream narrative talk about moral hazard much anymore. It’s embarrassing for many to acknowledge they thought the Fed would actually a number of banks fail on the basis of reputational integrity (ha!). So we ignore that we thought that, we slowly change our assumptions about the way they will behave, and we drive on.

No one cares or talks about this anymore. Nothing to see here. A perfect example of a narrative losing Attention, even though ‘price stability’ is one of the Fed’s dual mandates’

“Who controls the past controls the future. Who controls the present controls the past”

“The past was erased, the erasure was forgotten, the lie became the truth”

What we are facing now is much more dangerous than the seemingly natural Alzheimers that institutions go through. Forgetting the lessons of history slowly is like a trench-warfare. What we are facing now is the nuke dropped on the trenches that happens in an instant and no one sees it coming until it’s too late.

As with Orwell’s Newspeak, controlling language is the thoroughfare to control of ideas. Consider how many of Alinsky’s ‘Rules for Radicals’ concern narrative dominance. The SJW’s know this. The politicians and the corporate oligarchy know this, and technology has allowed them the means to scale their efforts in ways that would have made Oceania’s Inner Party jealous. We can rename old ideas into acronyms like MMT, rebranded and repackaged for the nudging-turned-shoving state and elite to use. It’s a function of the modern zeitgeist, not a flaw, that we can barely agree on basic facts. Orwell’s memory hole exists in institutions all around us. Cue the Neuralyzer.

Reformat and Rewrite

So what happens next? More of the same - more rewriting of institutional memories, more financialization, less subtle and more overt nudging by the state and oligarchy toward what they want you to think. More cognitive dissonance between the ideas that we have about institutions and what they are actually going to be doing. That in itself is a powerful weapon for the state and the elite - it at least gives them cover for a while, until people figure it out, and then it’s too late for them. And then inflation, which with its consequences, has components of both computational irreducibility (a model or formula cannot solve for) and radical uncertainty - we can’t even imagine what we should be worried about. But we won’t, because we can’t.